As your Houston real estate expert, I’ve seen this city through every cycle imaginable—from the “wild west” bidding wars of years past to the steady, strategic market we are navigating today in May 2026. If you’ve been scrolling through Zillow or driving through The Heights, Katy, or Sugar Land, you’ve likely noticed something: the “wait and see” approach isn’t the strategy it used to be.

The 2026 Houston market is finally giving us some breathing room. Inventory is balanced, and while interest rates aren’t back to the 3% “fairytale” levels, they have stabilized into a range that makes homeownership a very real possibility for those who know how to play their cards right.

Choosing your financing isn’t just about the lowest number; it’s about which tool fits your specific Houston lifestyle. Let’s dive into the FHA, VA, and Conventional landscapes for 2026.

The 2026 Rate Landscape: Where Do We Stand?

Before we talk about loan types, let’s look at the numbers. As of mid-May 2026, Houston is seeing a fascinating stabilization. Here is the general “vibe” of the current rates:

Conventional 30-Year Fixed: Hovering between 6.1% and 6.4%.

FHA 30-Year Fixed: Slightly lower, often around 5.8% to 6.1% (but remember that MIP!).

VA 30-Year Fixed: The winner for our veterans, currently sitting near 5.6%.

While these numbers are higher than the 2021 lows, they are a far cry from the volatility of 2023. In Houston, where the median home price is currently around $335,000, these rates mean a manageable monthly payment for a beautiful single-family home in growing areas like Cypress or Spring Branch.

1. FHA Loans: The First-Time Buyer’s Best Friend

FHA loans remain a powerhouse in the Houston market. In 2026, I am seeing more clients use FHA to break into neighborhoods where prices have stayed resilient.

Why FHA in 2026?

Lower Down Payment: Still the gold standard at 3.5%. For a $330,000 home in Humble, that’s only $11,550 down.

Credit Flexibility: If your credit score took a small hit during the economic shifts of 2025, FHA is much more forgiving than Conventional.

Assumability: This is the “hidden gem” of 2026. FHA loans are generally assumable, meaning if you sell your home in a few years, a buyer could potentially take over your 6% rate even if market rates have climbed to 8%.

Aida’s Tip: Don’t forget the Mortgage Insurance Premium (MIP). Unlike Conventional loans, FHA insurance usually stays for the life of the loan. We need to run the math to see if refinancing into a Conventional loan makes sense once you hit 20% equity.

2. VA Loans: Honoring Our Texas Heroes

Houston has a massive veteran population, and the VA loan is, quite frankly, the best mortgage product on the planet. If you served, you’ve earned this.

The 2026 VA Advantage in Houston:

0% Down Payment: No other loan lets you keep your cash in the bank quite like this.

No Monthly PMI: This saves you hundreds every single month compared to FHA or low-down-payment Conventional loans.

Texas Tax Perks: Don’t forget that in Texas, if you have a 100% disability rating, you may be eligible for a full property tax exemption. In a city like Houston where property taxes hover around 1.8% to 2.1%, that is a life-changing amount of money.

3. Conventional Loans: The Flexible Giant

Conventional loans are for my buyers with strong credit (720+) or those who want to avoid the “red tape” sometimes associated with government-backed loans.

What’s new in 2026?

The Conforming Loan Limit for 2026 has increased to approximately $832,750. This means you can buy a luxury property in Memorial or River Oaks using a standard Conventional loan without needing a more complex (and expensive) Jumbo loan.

Why choose Conventional?

No PMI with 20% down: Or, if you put down 5%, the PMI automatically cancels once you hit 80% Loan-to-Value (LTV).

Appraisal Ease: Conventional appraisals are often faster and less “picky” about minor repairs compared to FHA or VA.

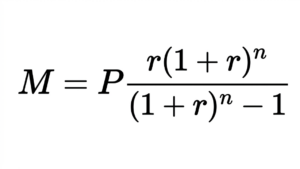

Let’s Talk Math

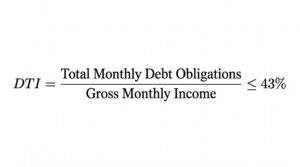

When we sit down to look at your budget, we don’t just look at the home price. We look at the Debt-to-Income (DTI) ratio. To calculate your maximum monthly payment, we generally want your total debt (including the new mortgage) to be:

In Houston, we also have to account for our property taxes and homeowners’ insurance (which, let’s be honest, has seen some hikes recently). A typical monthly payment formula for a fixed-rate mortgage looks like this:

Where:

M = Total monthly payment

P = Principal loan amount

r = Monthly interest rate (annual rate divided by 12)

n = Number of months (e.g., 360 for a 30-year loan)

Don’t worry—I have a spreadsheet that does this for us so you can focus on picking out paint colors!

Frequently Asked Questions

What is the current mortgage rate in Houston, TX for 2026?

Currently, rates are averaging between 5.6% (VA) and 6.4% (Conventional). These vary based on your credit score and down payment.

Is it a good time to buy a house in Houston right now?

Yes. Unlike 2023-2024, the market in 2026 has more inventory. You have more leverage as a buyer to ask for repairs or closing cost credits, which were unheard of a few years ago.

What is the 2026 conforming loan limit for Harris County?

The baseline conforming loan limit for 2026 is approximately $832,750 for a single-family home.

Can I get a VA loan with 0% down in Houston?

Absolutely. If you have your Certificate of Eligibility (COE) and meet the service requirements, you can purchase a home with no down payment and no monthly mortgage insurance.

How much are property taxes in Houston in 2026?

Effective tax rates typically land between 1.8% and 2.1% of the market value. However, thanks to the 2025 Homestead Exemption increase (Proposition 13), the school district exemption is now $140,000, providing significant relief for homeowners.

Final Thoughts: Your Houston Journey Starts Here

Navigating the financial side of real estate can feel like trying to drive on I-45 during rush hour—stressful and confusing. But it doesn’t have to be. Whether you are looking for your first home in The Woodlands or upgrading to a larger space in Fulshear, the right financing is the engine that gets you there.

As your Realtor, I am here to do more than just open doors. I am here to ensure you are making a move that builds long-term wealth.

Ready to see what you qualify for in today’s market? Let’s connect. Whether it’s FHA, VA, or Conventional, we’ll find the path that leads you home.

Aida Villalobos | Real Estate Broker

📞(346) 955-1049

Disclaimer: I am a licensed Real Estate Agent in the State of Texas. I am not a mortgage lender. Interest rates and loan programs are subject to change based on market conditions and individual creditworthiness. Always consult with a licensed mortgage professional for specific financial advice.